How do I measure distance to coast?

When to Measure Distance to Coast

Which Bodies of Water Count as "Coast"

How to Measure Distance to Coast

Overview

Accurate distance-to-coast measurements help you avoid declined submissions, mid-term policy changes, and surprise deductibles. Many property carriers base eligibility, pricing, and wind or hurricane deductibles on how far a building sits from the ocean or other large bodies of water. When you enter distance accurately, underwriters can quote faster and more confidently.

When to Measure Distance to Coast

You'll typically need an accurate distance when:

The property is in a coastal state (Alabama, Florida, Georgia, Louisiana, South Carolina, North Carolina, Texas, etc.) or along the Great Lakes or other major bodies of water like Lake Pontchartrain and Lake Borgne.

Carrier appetite mentions distance limits such as "within X miles of the coast" or "wind excluded inside X miles."

You see separate wind, named storm, or hurricane deductibles in quotes—common for coastal homes and commercial properties.

If the building is obviously far inland (more than 30 miles from the ocean or Gulf), most carrier tools treat it as non-coastal, and detailed distance measurement may not be required.

Which Bodies of Water Count as "Coast"

For most property guidelines, "coast" means:

Open ocean or gulf shoreline

Great Lakes shoreline

Major bodies of water that generate coastal wind and storm surge (oceans, bays, sounds, intracoastal waterways, large lakes)

Other Bodies of Water

Bays, sounds, and intracoastal waterways: Many vendor tools treat these as part of the coastline for wind and storm-surge exposure. Measure to the edge of that water, not only to the open ocean.

Rivers and lakes near the ocean: Some inland bodies of water still create coastal-type wind and surge exposures. Carrier guidelines may specify which water bodies count.

Barrier islands: For homes and businesses on barrier islands, the distance to the coast is often effectively zero. They are treated as top-tier wind exposure by most E&S carriers.

When in doubt: Measure to the nearest large body of water labeled on Google Maps (typically anything marked as a bay, sound, ocean, or Great Lake) that could realistically drive hurricane or coastal storm winds. You can also contact your Account Manager.

How to Measure Distance to Coast

Google Maps Method (2-3 minutes)

Many agents use Google Maps to get a reliable distance in a few steps.

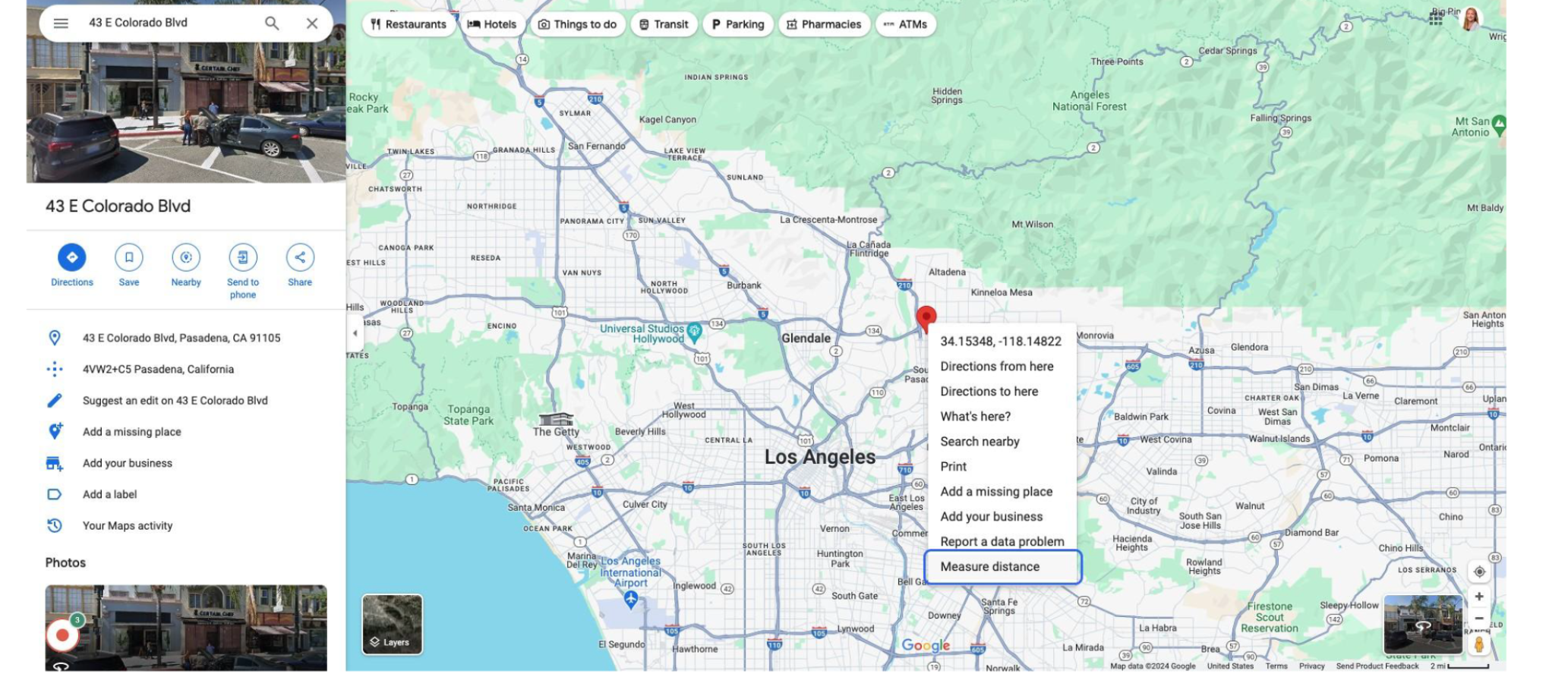

Enter the street address and right-click the building and choose Measure distance.

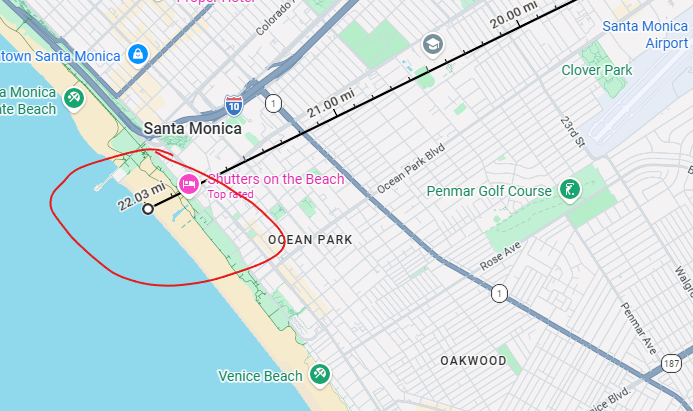

Scroll or drag to the nearest coastline (ocean, gulf, or large bay/sound) and click once more.

Use the straight-line distance shown in feet or miles as your distance to the coast, as carriers and vendor tools calculate the shortest straight-line (as-the-crow-flies) distance from the structure to the coastline, not driving distance.

Pathpointer: Zoom in closely so you're measuring from the actual building footprint, not the center of the ZIP code or town. This matches how carrier tools work and avoids being off by several hundred feet.

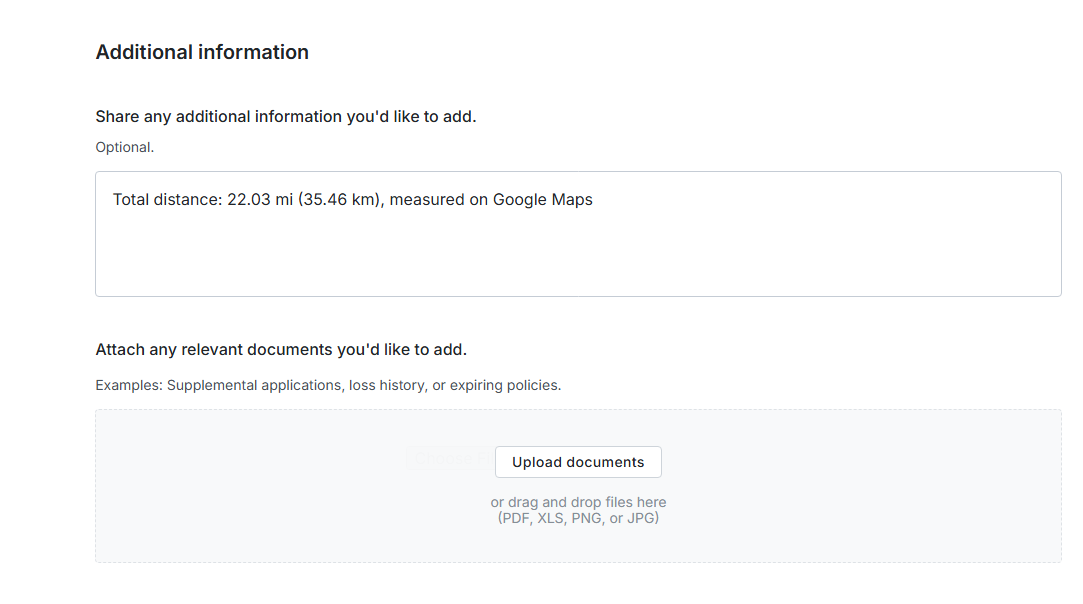

Add the distance in-app when you're submitting. Under Additional Information, you can note how you measured (e.g., "0.8 miles to Gulf via Google Maps"). If needed, upload a screenshot of the map for clarity.

Underwriter Methods

For high-value or complex coastal properties, our team relies on geocoding and distance-to-coast data from insurance-grade vendors such as Verisk's LOCATION Distance to Coast and MapRisk. These tools use GIS and proprietary coastline definitions to measure distances within a few feet.

Underwriters use this data to:

Decide if a risk is within or outside a coastal or wind pool zone

Apply the right wind or hurricane deductible, or exclude wind entirely

Flag submissions for catastrophe modeling or referral if they fall within specific distance bands (e.g., inside 1 mile, 1–5 miles, 5–10 miles)

Your manual measurement helps us get in the right ballpark and reduce surprises, but final underwriting decisions will use these precise tools.

Miles vs Exposures

Deductibles and coverage considerations vary by carrier. Note: These ranges are general guidelines only and vary by carrier:

Inside 1 mile of open ocean: Higher wind exposure; separate wind or named-storm deductibles are common.

3–5 miles from the coast: Moderate wind exposure; separate wind deductibles may apply, though more carriers are willing to quote.

More than 10 miles inland: Lower wind exposure; standard coverage is more typical, though local wind pool zones may still apply.

FAQs

Do I need to measure for every submission in a coastal state?

Only when the property is close enough to the coast that wind exposure could affect eligibility or pricing. Properties clearly inland (30+ miles) typically don't require precise measurement.

What if I'm not sure which coastline to use?

Measure to the nearest large body of water (typically anything labeled on Google Maps as a bay, sound, ocean, or Great Lake) that could generate coastal wind exposure. When in doubt, estimate conservatively (a shorter distance) and note it in the submission under Additional Information.

Does distance to coast affect every coastal property?

No, only properties within certain distance thresholds (typically within 10–15 miles of the coast) will see pricing or coverage adjustments based on this measurement.

What if my manual measurement differs from the carrier's calculation?

Carriers use insurance-grade geospatial tools that may produce slightly different results. Your estimate helps us pre-screen the risk, but the carrier's final calculation determines pricing and coverage. Any significant discrepancies will be flagged during the inspection or underwriting review.

What if Google Maps isn't giving me an accurate measurement?

If you're having trouble with the measurement tool or the property is in a complex coastal area (multiple bays, inlets, or barrier islands), note your best estimate in Additional Information and flag it for underwriter review. Our team can verify using professional tools.

Related Articles

Does Pathpoint provide monoline wind coverage?

What information do I need for a property quote?